{kind=link}

From 2020 through mid-2026, the tech industry cut over 950,000 jobs — but the narrative that it was one continuous downturn is wrong.

There were six distinct waves, each with a different cause, a different cohort of victims, and a different signal for what comes next. Understanding tech layoffs by year is not a history lesson — it is a leading indicator for hiring, valuation, and where the next opportunity window opens.

Tech Layoffs by Year: The Complete Data

Data sourced from Layoffs.fyi, WARN Act filings, and company announcements. Numbers represent total reported cuts per calendar year across public and private technology companies.

| Year | Approx. Layoffs | Primary Driver | Largest Cuts |

|---|---|---|---|

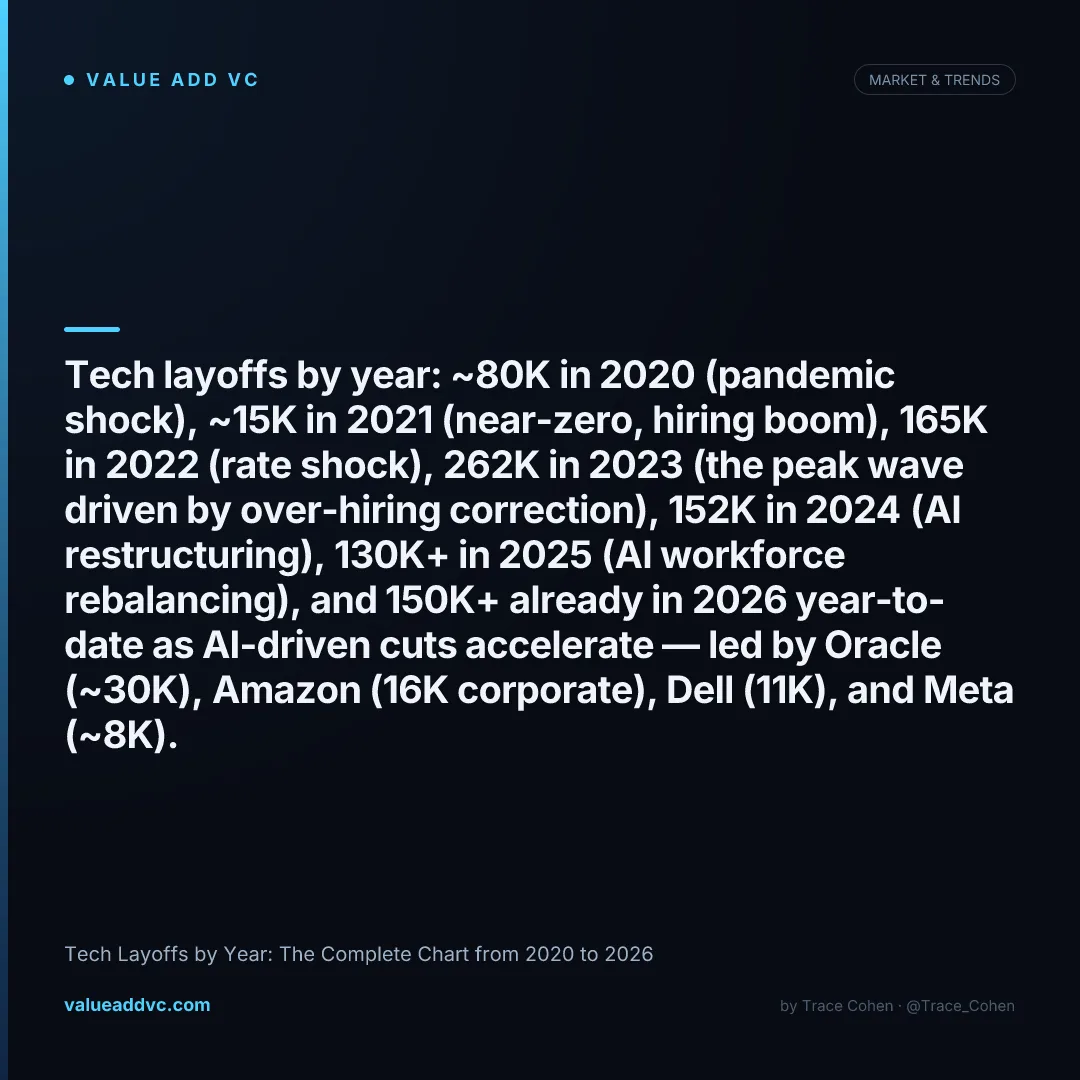

| 2020 | ~80,000 | Pandemic shock (travel, retail, media) | Uber, Airbnb, Yelp, TripAdvisor |

| 2021 | ~15,000 | Near-zero — peak hiring boom | Scattered smaller cuts only |

| 2022 | ~165,000 | Rate shock + revenue slowdown | Meta 11K, Twitter 3.7K, Stripe 14%, Lyft 13% |

| 2023 | ~262,000 | Over-hiring correction + margin pressure | Amazon 18K, Google 12K, Meta 21K, Microsoft 10K |

| 2024 | ~152,000 | AI restructuring + continued rationalization | Google 12K, Amazon 14K, Intel 15K+, Cisco 4K |

| 2025 | ~130,000+ | AI workforce rebalancing | Intel 15K, Workday 8.5%, Salesforce 8K, Dell 10% |

| 2026 YTD | ~150,000+ | AI-cited cuts accelerate (55% of events) | Oracle ~30K, Amazon 16K, Dell 11K, Meta ~8K |

| Total | ~954,000+ | Cumulative through June 2026 | 2022–2024 = 579K alone |

Breaking Down Each Wave

2020 — Pandemic Shock (~80K)

The 2020 cuts were concentrated in consumer-facing tech companies exposed to lockdowns: Uber cut 14% of its workforce (3,700 people), Airbnb 25% (1,900), and Yelp 17%. Enterprise SaaS was barely touched. This wave was fast and sharp — most companies that cut in Q2 2020 were hiring aggressively again by Q4 2020. It is the anomaly in the five-year chart, not the start of a trend.

2021 — Near-Zero Layoffs (~15K)

2021 was the peak hiring boom. Flush with zero-rate capital, tech companies added headcount at an unprecedented rate. Meta added 28,000 employees, Amazon 310,000, and Google over 20,000. Layoffs were effectively nonexistent. This over-hiring planted the seed for the 2022–2023 correction. The companies that hired the most in 2021 cut the most in 2023.

2022 — Rate Shock Hits (~165K)

The Fed raised rates 425 basis points in 2022. Multiples compressed overnight — median public SaaS EV/Revenue fell from 15x to under 5x. Recruiting froze, then cuts started. Meta's November 2022 11,000-person cut was the single largest in tech company history at the time. Stripe, Lyft, and dozens of mid-stage startups followed. The 2022 wave was mostly about valuation shock and investor pressure on margins.

2023 — The Peak Wave (~262K)

2023 was the largest single year for tech layoffs in recorded history. Amazon cut 18,000 in January alone. Google announced 12,000 cuts (6% of global workforce) in the same week. Meta added a second wave of 21,000 cuts on top of its 2022 round. The driver was plain: these companies had doubled headcount in 24 months and needed to prove to investors that they could operate at efficiency. The layoffs were not about the business failing — Meta's revenue grew 16% in 2023 while it was cutting thousands of people.

2024 — AI Restructuring (~152K)

The 2024 wave was qualitatively different. Intel announced a historic restructuring — 15,000+ cuts tied to losing market share to TSMC and AMD. Cisco cut 4,000 as networking hardware commoditized. SAP, Workday, and UiPath all reduced workforces while simultaneously hiring AI engineers. For the first time, layoff announcements explicitly cited AI as a reason: roles being automated, redeployed, or eliminated through tooling. This is a workforce rebalancing, not a headcount reduction.

2025 — AI Rebalancing Continues (~130K+)

In 2025, cuts were more targeted. Intel's second restructuring wave (15K), Workday (8.5% of workforce), Dell (10%), and Salesforce (8,000) all eliminated layers of middle management, customer support, and legacy product teams. Simultaneously, OpenAI, Anthropic, xAI, and AI infrastructure companies posted aggressive hiring. The labor market bifurcated: those who can build and deploy AI are in unprecedented demand; everyone else is facing reduction.

2026 — The Acceleration (~150K+ YTD)

2026 opened with the fastest pace of cuts since 2023. Oracle executed the largest single layoff of the year (estimated 20K–30K in March), Amazon cut 16,000 corporate roles in January, Dell shed 11,000 (roughly 10% of its workforce), and Meta announced an ~8,000-person reduction in April — with Meta and Microsoft's combined 20K cuts prompting open debate about an AI-driven labor crisis. By early June, trackers counted 150K+ workers cut across 500+ companies, and 55% of layoff events explicitly cited AI or automation. At the current rate, 2026 could rival or exceed 2023's record 262K.

The Pattern Behind the Tech Layoffs Chart

Each wave had a cause — but the 2022–2024 peak was ultimately a hangover from 2020–2021 zero-rate exuberance. Here is what the data actually shows:

579K

Cuts in 2022–2024 alone

Largest 3-year downsizing in tech history

25%

Layoffs from 7 companies

Meta, Amazon, Google, Microsoft, Salesforce, Intel, Cisco

2023

Peak year by volume

262K cuts — 60% more than any prior year

The Cumulative View: Workers and Companies by Year

Looking at the same data through a cumulative lens — including how many companies cut each year — shows how broad each wave was, not just how deep.

| Year | Workers Laid Off | Companies |

|---|---|---|

| 2022 | ~165,000 | 1,040+ |

| 2023 | ~262,000 | 1,190+ |

| 2024 | ~152,000 | 640+ |

| 2025 | ~130,000+ | 500+ |

| 2026 YTD | ~150,000+ | 500+ |

Source: Layoffs.fyi and company announcements. 2026 YTD through early June 2026.

The biggest single-company cuts of the 2023 record year, for context: Amazon 27,000+ across two tranches (~9% of corporate staff), Google 12,000 (~6% of headcount), Meta 10,000 in its second round, Microsoft 10,000, Salesforce 8,000, and Dell 6,650. Nearly a million cumulative layoffs sounds catastrophic — in context, it is a forced correction after an equally extreme hiring surge. From 2020 to 2022, the top 10 tech companies added roughly 500,000 net employees. The reversal is painful but arithmetically predictable.

What is Normalizing

- ✓ Revenue-per-employee metrics improving across Big Tech

- ✓ Operating margins recovering toward pre-2020 levels

- ✓ VC-backed company burn discipline higher than 2021

- ✓ Fewer companies hiring purely on growth optionality

What is Still Structural Risk

- ✕ AI-driven role elimination has no natural ceiling

- ✕ Mid-level roles are now under pressure, not just junior

- ✕ Remote-first hiring reversed — reducing talent pool access

- ✕ Startup hiring still highly selective at seed and A

What This Means for Founders and Investors

I have backed over 65 companies across the last decade. The layoffs data tells a specific story for early-stage operators:

Senior talent is available at reasonable comp — for now

The 2022–2024 waves flushed experienced engineers, PMs, and operators into the market. Most found new roles, but mid-level and senior talent remains more accessible than it was in 2021. This window will not last — the next hiring cycle is starting.

The AI restructuring creates a specific hiring opportunity

Companies cutting legacy ops and support roles are creating a supply of intelligent, process-oriented generalists who understand enterprise workflows. These are exactly the profiles early-stage companies need for implementation, customer success, and ops roles.

Survival bias in layoff rounds is real

The people who were not cut in 2023 are, statistically, the best performers at those companies. The talent who survived four rounds of cuts at Meta or Amazon is unusually good. Recruiting from post-layoff teams is still a high-signal strategy.

The 2022–2024 wave was the correction. The 2025–2026 wave is something different.

It is not about too many people. It is about the wrong people for what comes next.

Track live tech layoff data on the Layoffs Dashboard and monitor the hiring counter-trend on the Hiring Tracker at Value Add VC. Originally published in the Trace Cohen newsletter.

Get VC data most people never see

— 100% free

Weekly benchmarks, valuations, and fund data. Join 5,000+ investors. No spam.