{kind=link}

If you searched for AAPL, MSFT, GOOGL, AMZN, or NVDA EPS in 2022 vs 2023, the short answer: Nvidia 7x'd in a year, and that was just the start of the most polarized big-tech earnings divergence in a decade.

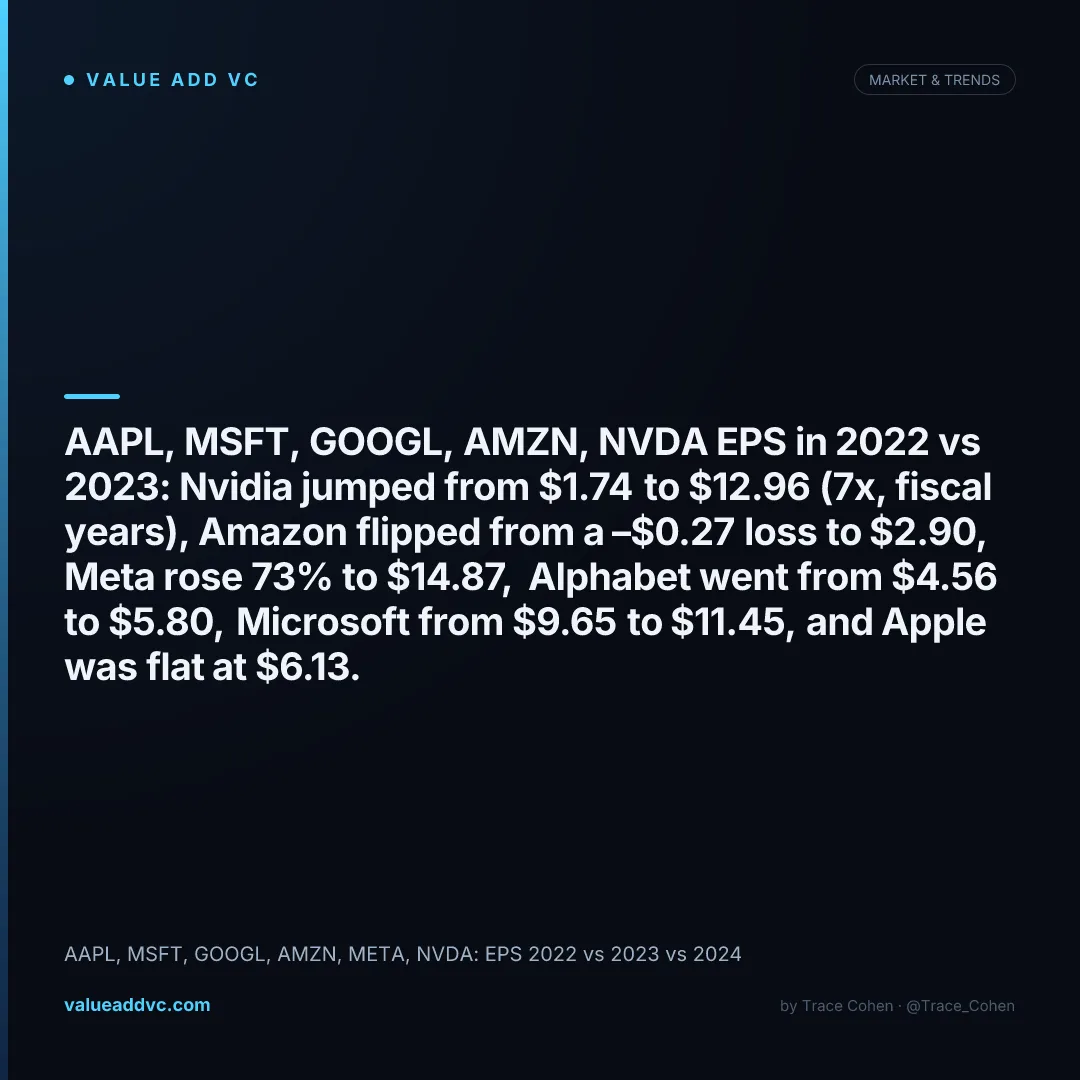

From 2022 to 2023, Nvidia's EPS jumped from $1.74 to $12.96 (fiscal years), Amazon flipped from a –$0.27 loss to $2.90, and Meta rose 73% to $14.87 — then by 2024 Nvidia hit $29.76, a 17x increase across two fiscal years. Meanwhile Apple ground out 5% total EPS growth across the same stretch. This is not a sector story — it's a company-by-company story about positioning versus the AI capex cycle.

AAPL, MSFT, GOOGL, AMZN, META, NVDA: EPS by Year

Note: Nvidia's fiscal year ends in January. FY2023 = Feb 2022–Jan 2023; FY2024 = Feb 2023–Jan 2024; FY2025 = Feb 2024–Jan 2025. All others are calendar year.

| Company | EPS 2022 | EPS 2023 | EPS 2024 | 2-Yr Change |

|---|---|---|---|---|

| NVDANvidia | $1.74* | $12.96* | $29.76* | +17.1x |

| METAMeta | $8.59 | $14.87 | $23.86 | +2.8x |

| AMZNAmazon | –$0.27 | $2.90 | $5.53 | Flipped |

| GOOGLAlphabet | $4.56 | $5.80 | $8.04 | +76% |

| MSFTMicrosoft | $9.65 | $11.45 | $12.41 | +29% |

| AAPLApple | $6.11 | $6.13 | $6.42 | +5% |

*Nvidia fiscal year. FY2023 ends Jan 2023; FY2024 ends Jan 2024; FY2025 ends Jan 2025. Sources: SEC 10-K filings, Bloomberg.

Revenue Growth: Who Is Actually Getting Bigger

| Company | Revenue 2022 | Revenue 2024 | 2-Yr Growth |

|---|---|---|---|

| NVDA | $26.9B* | $130.5B* | +385% |

| AMZN | $514B | $638B | +24% |

| MSFT | $198B | $245B | +24% |

| GOOGL | $282B | $350B | +24% |

| META | $116B | $164B | +41% |

| AAPL | $394B | $391B | –1% |

*Nvidia FY2023 (ends Jan 2023) and FY2025 (ends Jan 2025). Apple revenue declined slightly due to China headwinds and iPhone mix. See how these public tech companies compare to IPO-stage valuations on our tech IPO tracker.

What Drove the Divergence

Nvidia

AI GPU monopoly pricing. H100 and Nvidia's latest GPUs ASPs of $25K–$40K per unit with 60%+ gross margins. Every hyperscaler and frontier AI lab is a captive buyer.

Meta

Year of Efficiency: headcount cut from 87K to 67K in 2023, then held flat while revenue accelerated. AI-driven ad targeting lifted CPMs. Operating margins expanded from 20% to 41%.

Amazon

AWS margin expansion drove the swing from loss to $5.53 EPS. AWS operating income grew from $22.8B in 2022 to $39.8B in 2024. Retail segment restructuring reduced fulfillment costs by $5B+.

Microsoft

Azure AI revenue integration (Copilot, OpenAI partnership) added ~$4B in incremental revenue by 2024. Steady compounding on cloud re-signed contracts. EPS grew reliably but without a step-change.

Alphabet

2022 was an advertising recession year. The 2023–2024 recovery combined with YouTube growth and Google Cloud crossing $11B quarterly revenue drove EPS nearly doubling from the 2022 trough.

Apple

China revenue headwinds, iPhone ASP plateauing, and lack of a generative AI hardware catalyst kept growth muted. Services grew to 24% of revenue but couldn't offset hardware stagnation.

Margins Tell the Real Story

EPS can be gamed with buybacks. Operating margin expansion is harder to fake — it reflects real structural improvement.

Efficiency reset + AI ad targeting

AI GPU premium pricing power

AWS mix shift + fulfillment restructuring

Steady; Copilot uplift still building

Ad market recovery + cloud scale benefits

Services mix improving but hardware drag remains

What This Means for Investors and Founders

Three things I take from this data as a VC who watches these numbers closely:

Nvidia is a capex proxy, not a product company

NVDA's earnings are not sustainable at the 2024 growth rate. They are a direct readthrough for AI infrastructure spend. When hyperscalers pull back capex — and they will, eventually — Nvidia's EPS will compress faster than its revenue.

Meta is the best-managed big-tech stock of the cycle

Going from 87K employees to 67K while nearly tripling EPS is a masterclass in corporate efficiency. Most companies that cut headcount 23% see culture destruction and revenue miss. Meta tightened and accelerated. That's rare.

Apple's flat EPS is a warning signal for hardware-first models

When you have 98% brand loyalty and still can't grow EPS by more than 5% over two years, the hardware plateau is real. Services are good but not enough. The AI hardware supercycle will be crucial — if Apple misses it, the flat line gets worse.

The EPS divergence between these six companies is not noise.

It is a signal that AI infrastructure positioning — not legacy moats or brand strength — is now the primary driver of earnings growth for the next decade.

Track real-time big tech earnings multiples on the Big Tech Earnings Dashboard.

Data sourced from SEC 10-K filings and Bloomberg consensus. Nvidia fiscal years noted separately. Originally published in the Trace Cohen newsletter.

Get VC data most people never see

— 100% free

Weekly benchmarks, valuations, and fund data. Join 5,000+ investors. No spam.